For more than a decade, PAYGo transformed access to essential services across Africa. It proved something incredibly powerful: that consumers previously excluded from traditional finance were not unbankable—they were simply underserved by the wrong infrastructure. Solar home systems became the gateway product. With flexible mobile money repayments and remote device control, millions of households gained access to electricity for the first time. PAYGo was not just a financing model; it became the foundation of a new economic engine across emerging markets.

But success created a dangerous assumption.

Many operators began to believe that the same systems built to manage PAYGo solar could support the future of all financed businesses. That assumption is now becoming one of the biggest barriers to growth across the continent.

Because today, businesses are no longer financing a single product. They are financing entire ecosystems.

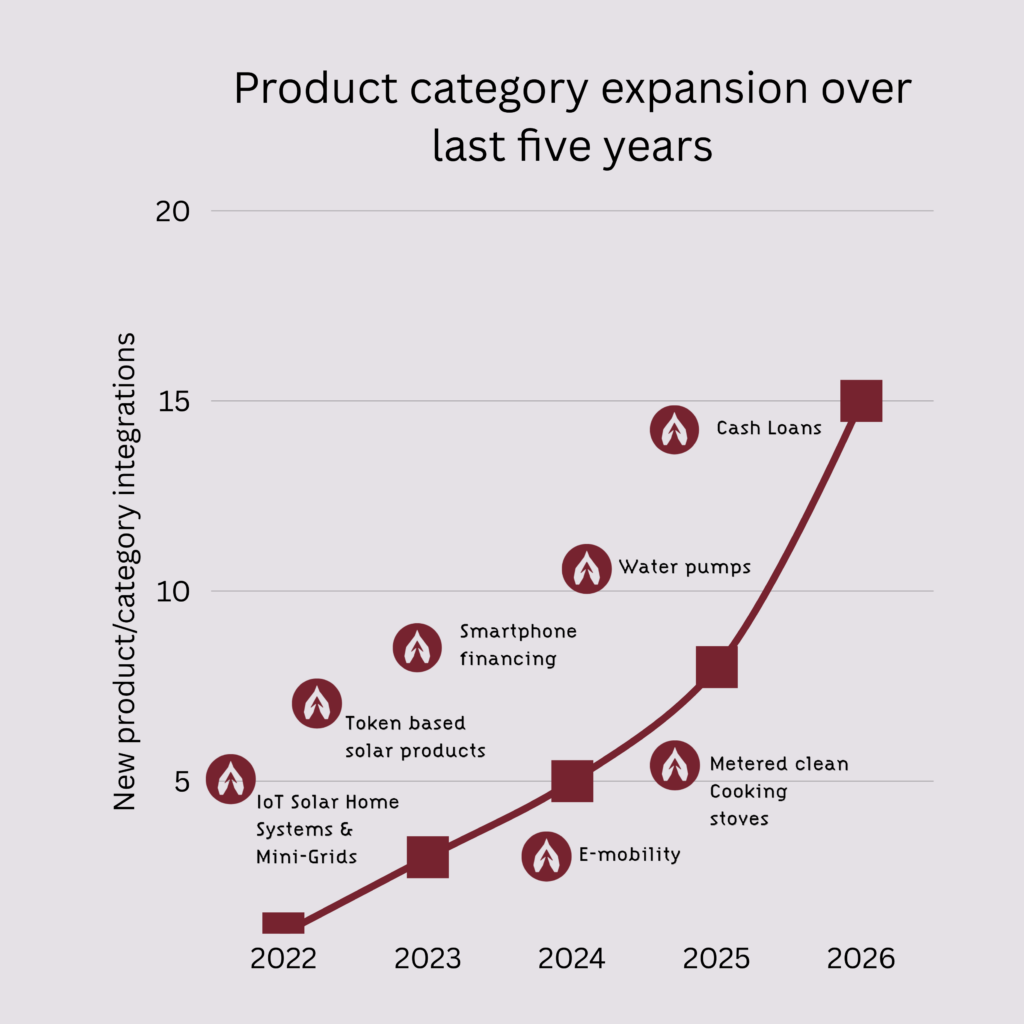

The modern financed economy looks very different from the early PAYGo years. A customer who once entered the system through a solar home system may now need a smartphone for connectivity, clean cooking for household efficiency, a water pump for agricultural productivity, e-mobility for transport, and access to working capital through embedded credit or cash loans. The customer journey is no longer linear, and the financing model is no longer single-product. Operators are managing portfolios that span physical assets, digital services, and financial products simultaneously.

Yet many of the platforms still powering these businesses were built for a world that no longer exists.

Legacy PAYGo platforms were designed brilliantly for one problem: managing solar repayment plans. They were built around a simple logic—one customer, one device, one repayment structure, one asset lifecycle. That model worked exceptionally well for solar home systems and entry-level energy products. But once businesses begin to diversify, the cracks start to appear.

A platform built for one product struggles when the same customer now holds multiple financed relationships. One repayment schedule becomes several. One billing unit becomes many—days, kilowatt hours, LPG refills, monthly subscriptions, loan repayments, device instalments. One customer profile becomes a complex financial ecosystem. What was once a clean repayment model becomes operational friction hidden inside spreadsheets, disconnected apps, and manual reconciliation processes.

This is the PAYGo trap.

It is not a problem of demand. Demand across Africa for financed access to essential services is enormous and growing. The challenge is operational infrastructure. Scaling from 5,000 financed assets to 500,000 is not a sales problem—it is a systems problem. Device status becomes unclear. Repossession workflows break down. Collections become inconsistent. Field teams lose visibility. Credit decisions rely on incomplete information. Revenue leakage increases silently while management teams continue to believe the problem sits in customer acquisition.

In reality, the problem is that most businesses are trying to scale modern financing models on outdated operational architecture.

This is a lesson Bboxx learned early.

Since 2010, Bboxx has built one of Africa’s most advanced distributed operations businesses, starting with clean energy and expanding far beyond it. Solar was never the final destination—it was the entry point. Access to energy unlocked the opportunity to finance broader economic mobility. Customers who trusted Bboxx for solar could now access smartphones, clean cooking solutions, water pumps, e-mobility, and broader financial services. The financing relationship deepened. The portfolio became more valuable. But the operational complexity increased exponentially.

The challenge was never whether these products could be financed. It was whether the business could manage the complexity of financing them at scale.

How do you reconcile millions of mobile money payments across multiple providers and countries? How do you automate revenue recognition across different product categories? How do you track every financed asset from onboarding to repayment completion, including repossession, redeployment, and refurbishment? How do you coordinate thousands of field agents across low-connectivity environments while maintaining accountability and performance visibility? How do you move beyond static credit scores and make lending decisions based on real repayment behaviour, liquidity patterns, and behavioural signals?

Traditional PAYGo platforms could not solve this because they were never designed to.

So Bboxx built Pulse.

Pulse was not created as a software product for external sale. It was built as operational infrastructure to solve real problems inside one of Africa’s most complex distributed financing businesses. It became the digital backbone managing payments, assets, customer lifecycle, field operations, and credit intelligence across multiple sectors and geographies. Today, that platform has processed more than 100 million mobile money transactions, managed over 1 million financed products, and supported more than 6 million lives across Africa. It operates across more than 10 markets with over 20 payment provider integrations and 99.9% platform uptime.

That platform is now commercialised through Asopo Technologies.

This distinction matters because the market is crowded with software providers offering narrow solutions. Some are excellent PAYGo management tools. Others are global CRMs adapted for local markets. But very few are true operating systems built for mobile-money-first economies. PAYGo tools often remain trapped inside a single vertical. CRMs like Salesforce or Zoho offer power but ignore the realities of fragmented payment rails, device-linked credit, field collections, and distributed asset management. Businesses end up stitching together multiple systems that were never designed to work together.

The result is not scale. It is operational debt.

Every workaround creates another silo. Another spreadsheet. Another disconnected workflow. Another manual intervention required to keep collections moving. Leadership teams often do not see the problem immediately because the damage happens quietly. A delayed reconciliation here. A missed repossession there. A field team operating without live visibility. A borrower approved without enough behavioural insight. A one percent leakage in collections across a high-volume portfolio.

In asset finance, that one percent destroys margins.

This is why the next decade in African financing will not be won by the companies selling the most devices. It will be won by the companies that manage complexity better than everyone else.

The winners will understand that collections are not a finance function—they are a strategic growth engine. Credit scoring is not a dashboard feature—it is infrastructure. Field operations are not a support function—they are one of the largest drivers of EBITDA. Asset lifecycle management is not operational admin—it determines recovery rates, investor confidence, and long-term profitability.

Most importantly, they will understand that scale without operational control is not growth. It is delayed failure.

Africa does not need another PAYGo tool. It needs infrastructure.

It needs platforms that unify payments, assets, field operations, customer lifecycle, and credit intelligence into one operating system that can support businesses as they move beyond single-product financing into full ecosystem finance.

That is what Asopo was built to do.

Asopo is not another dashboard. It is not another repayment tool. It is not another CRM pretending to understand emerging markets. It is the infrastructure layer behind financed growth—built in the field, proven at scale, and designed for businesses that intend to move far beyond solar.

Because the next billion financed customers will not live inside one vertical.

Neither should your platform.